Published: 29 Sep 2020

4 post covid scenerios and how gold will perform

The coronavirus pandemic has caused a lot of uncertainty. But there is one thing that has not surprised economists and financial experts, and that is the steep rise in gold prices around the world.

As the coronavirus pandemic causes stock markets around the world to plunge, gold has once against proven its worth as a safe haven investment option, just as it did during the 2008 global economic crisis. This is because, in the long term, gold has a tendency to always be profitable, despite periods of deflation and inflation.

But there is more to understanding gold performance than decoding its price. To get a more specific idea about how gold could perform, you would have to hypothesize how a macro-economic situation- like a global pandemic- could impact the international supply and demand for gold.

To help you do this, the World Gold Council's Gold Valuation Framework- Quarum, a user-friendly web-based quantitative tool that lets you predict gold performance in different hypothetical scenarios can be used. Quarum lets you select pre-defined variables that may affect the global economy and thus, the performance of gold. Quarum allows you to:

- Leverage an academically validated methodology called the Gold Valuation Framework (GVF) to generate forecasts of demand and supply. GVF is a set of principles that helps you understand how various macroeconomic factors such as supply and demand can influence gold's performance.

- Calculate potential returns on gold investments over a period of 5 years or more.

Based on an analysis conducted by the World Gold Council using the GVF and data provided by Oxford Economics, here are four hypothetical economic situations that may arise post the coronavirus pandemic and gold's implied performance in each of them.

-

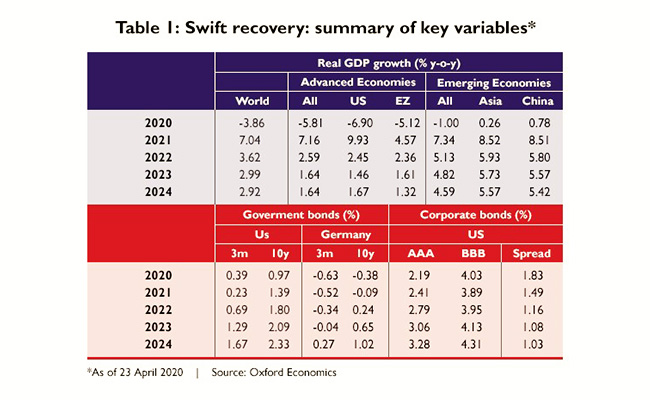

Swift economic recovery

When an economy revives quickly after facing a downturn, in the shortest possible time, the recovery type is V-shaped. This means that a sharp drop along the X and Y-axis is followed by a sharp rise due to strict economic measures taken proactively. Owing to the lockdown across different economies in the world, existing projections show that world GDP could contract by up to 4% in 2020, which is almost triple the decline that was seen during the 2008 global financial crisis.

A swift recovery is only possible if governments and central banks make monetary policies flexible and real interest rates remain close to zero between 2020 and 2024.

-

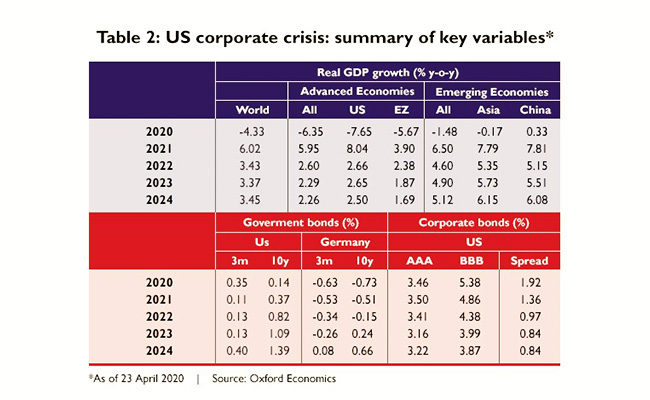

US corporate crisis

In this particular event, US corporations may take a downward deep dive. Wall Street stocks might plunge up to 45% in value, weakening the US dollar and consequently pushing up operating costs across US corporates. This, in turn, may have a negative impact on corporate profits and investor confidence in 2020. However, since most of the government policies support the promotion of the economy, projections show that by 2021, the US stock market will rise by 19% and the credit spread (which is the difference between the yield generated by US corporate bonds and treasury bonds. Both bonds have similar maturity but differ in credit quality) will narrow quickly. This recovery will be V-shaped as well.

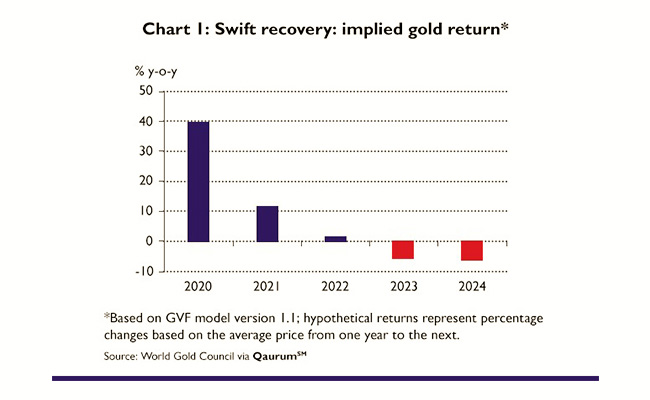

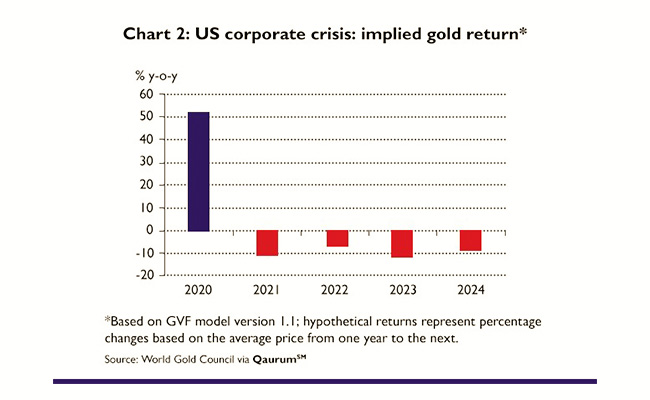

Gold's projected performance

This model assumes that gold's performance will fall for 4 straight years post-2020. However, the year on year returns between 2020 and 2025 is expected to remain positive at 2%. Investors, like you, will continue to buy gold as a hedge against market uncertainty amid falling stock prices. Better yields from government bonds and higher liquidity will impact gold's performance positively after 2021.

Related: The impact of US dollar on gold

-

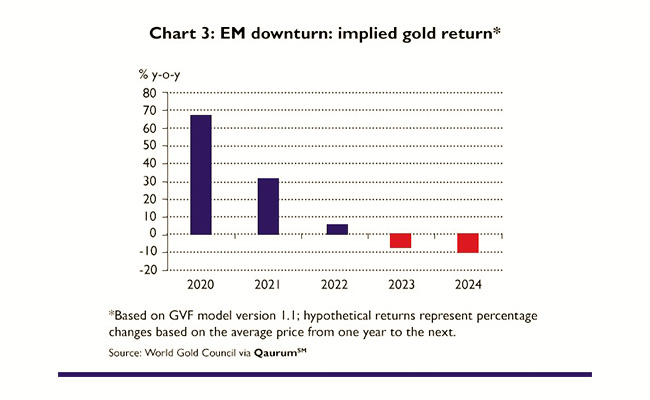

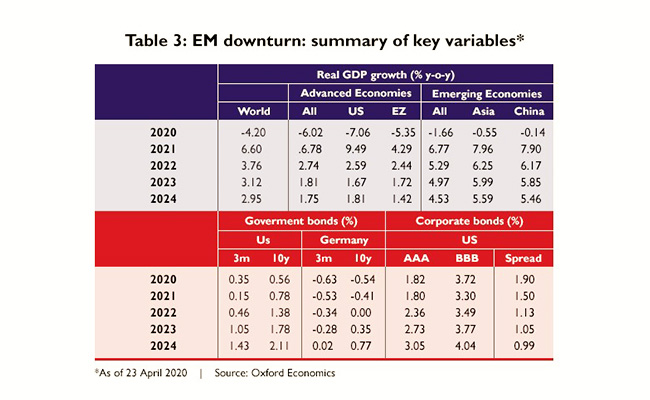

Emerging market downturns

This scenario presupposes that a contraction in the Chinese economy after 2020 will cascade to other emerging economies in Asia. The US and Western markets may perform relatively better. However, to prevent a global impact, central banks across the globe will have to initiate corrective measures by way of reducing interest rates over the long term. This will in turn control commodity prices, and stabilise the global market by 2021. This recovery is also V-shaped.

Gold's projected performance

Gold performance is expected to remain positive for 3 out of 5 years in this scenario, slowing down in 2023 and 2024. Annualised implied returns for the entire period between 2020 and 2024 are expected to show double-digit growth.

Similar to the earlier scenarios, the demand for gold falls after 2023 since higher consumer confidence will increase interest rates. The inverse relationship between gold's performance and its interest rate is underscored in this model.

-

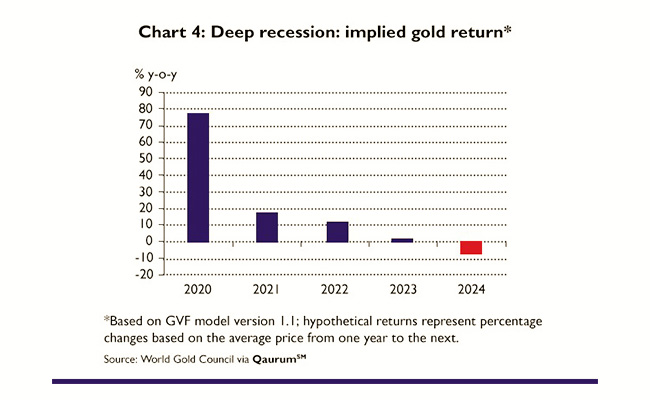

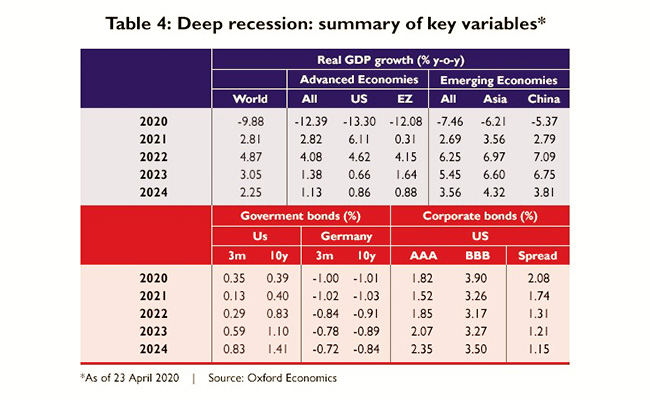

Deep recession

In case the global economy faces a deep recession as a result of the pandemic, the recovery will be U-shaped. Unlike a V-shaped growth curve, a U-shaped recovery is characterised by a period of no change along the X and Y-axis before it picks up rapidly. This scenario is likely in case it takes longer to fully open the world's economy by 2023, as planned. The delay can be potentially caused if the second wave of coronavirus infection comes in play. The brunt of this will be borne by advanced economies. In order to boost lagging growth, central banks around the world will have to persist with sub-zero interest rate regimes while yields from bonds and other debt instruments will continue to remain high through till 2024.

Gold's projected performance

Though gold performance remains fairly consistent from 2020 to 2023, it goes into the red in 2024. The annualised implied return throughout the 5 year period is expected to be approximately 20%. Gold performance is highest in 2020 on the back of higher anticipated risk which slows down considerably in 2023. This model stands out, particularly because the positive momentum built in 2020 in terms of gold performance carries over into the following year when interest rates are kept at levels close to zero. Beyond 2022, interest rates increase and with it, opportunity costs rise to cast a negative shadow on implied gold returns which continues through 2024.

Related: What makes gold the most useful commodity for investment?

Gold's projected outlook

The uncertainty surrounding the progression of COVID-19 will continue to make gold an attractive investment avenue as governments around the world aim to stimulate demand. Investors, like you, will look for better returns and opt for gold asset investments, in the face of falling stock valuations and overall demand contraction. Beyond that, much will depend on the effectiveness of government stimulus and fiscal policies.