Published: 29 Sep 2020

How does gold compare to other asset classes?

After high price volatility in the 1970s , gold returns reached a steadier level, making it clear why gold continues to generate potentially viable investment interest. Gold outperforms other asset classes in the long run, giving positive returns consistently across various market conditions.

Historically, gold has been a symbol of wealth and always in great demand. It was used as a currency even when coins of silver or bronze were in circulation. Demand for gold as an asset has been consistent and robust, buoyed by diverse segments such as:

- Central banks – which store gold as forex reserves

- Institutional investors – who see in gold a safe cushion amidst low interest rates under various monetary policies and concerns about the outlook for the dollar

- Individuals – who seek gold not only in the form of precious ornaments but also as investments for wealth accumulation and protection

Interestingly, gold has also been perceived as a liquid asset due to its inherent qualities:

- It is a soft metal and hence relatively easy to melt into ‘portable’ forms such as coins, bars, and ornaments (this made it different from other forms of traded goods such as cattle or grain)

- It does not degenerate (i.e., rust, decay, or lose lustre even after centuries – and its value is retained for a long time)

- Its supply is limited, making it rare and always in demand

- Its production is widely scattered and not concentrated in one geography; this keeps availability at levels high enough to generate interest

India's appetite for gold as an investment follows global trend

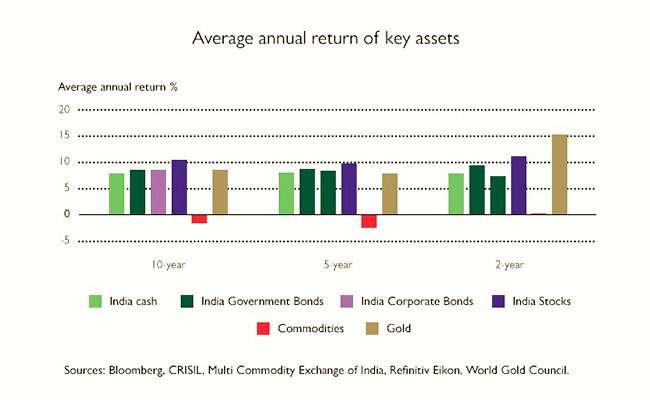

Gold has performed favourably against key asset classes such as bonds and stocks in India. Data on returns from various assets over periods of 2, 5, and 10 years (up to December 31, 2019) shows only stocks outperforming gold in the long run, though in the short term, gold ruled:

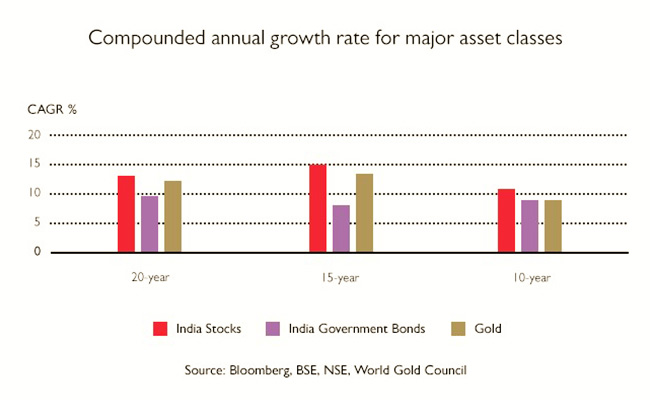

These facts have contributed significantly to the Indian investor’s love for gold. In terms of volatility in returns, gold sits below many individual stocks and stock indices and lower than individual commodities. In fact, gold’s compounded returns compare favourably with many asset classes, including stocks. It has outperformed even government bonds over a long-term period of 15 years and more. Since 2010 , gold has delivered positive annual returns most of the time and proved to be an effective portfolio diversifier in periods of highs and lows in the economy.

Related: How did the 2008 financial crisis impact gold? [Video]

Gold performs consistently

In these times of economic vicissitudes, gold has proven time and again that it is a safe-haven investment to hedge risks and mitigate losses. Of course, like any other economic asset, gold is susceptible to fluctuations over the short term. But what sets it apart from other investment assets is its proven track record in delivering positive returns – both during economic upturns and downturns.

Since 1981, gold has consistently beaten inflation with returns of 10% annually, on average, in India. In addition, the price of gold went up 11.5% on average in the years when inflation in India was more than 6%. In other words, gold preserved and helped capital growth over the long term, protecting investors against extreme inflation.

Another important point to consider is that gold also performs well during times of deflation. According to research findings at Oxford Economics, demand for gold during deflationary periods would be driven by low-interest rates, reduced consumption, decreased investment, and heightened financial stress.

Related: Why is gold considered a hedge against inflation?

Gold outperforms fiat currencies

Investor demand has been boosted by persistently low-interest rates and concerns about the outlook for the dollar, as these factors affect the perceived opportunity cost of holding gold. Historically, fiat currencies were pegged to gold until the collapse of the Bretton Woods system in 1971.

A fiat currency – such as the Indian rupee or the American dollar or the British pound – is a legal tender issued by the respective governments. Fiat money became the global norm after the collapse of the Bretton Woods monetary management system (where US-led Western powers, Australia, and Japan agreed to peg their currencies to gold). US President Richard Nixon decided to abandon this system, leading to the dollar delinking from gold; other countries followed suit.

Gold gives you purchasing power like a fiat currency, even though it is not legal tender. But compared with fiat currencies, gold is not impacted by economic uncertainties; in fact, gold benefits from inflows during periods of heightened risk. And since gold cannot be created, like the way paper currencies are printed, its supply has increased only by 1.6% a year for the past 20 years. What this has done is control a world gold glut eliminating any spectre of inflation.

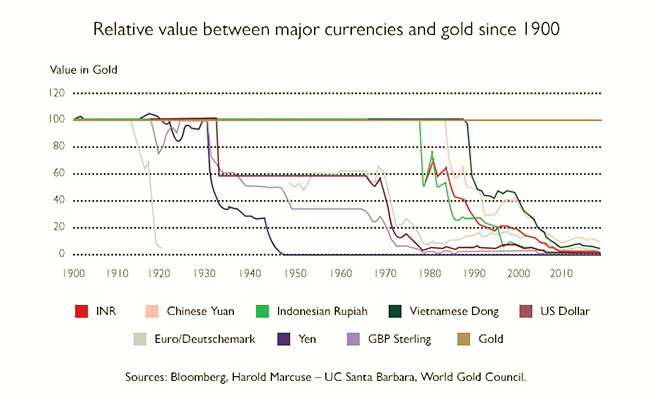

Gold has been well ahead of the various fiat currencies, outshining them consistently for over a hundred years.

Related: How is gold related to our currencies? [Video]

Data revealed by studies by Bloomberg, Prof Harold Marcuse of the University of California, Santa Barbara, and the World Gold Council shows that gold has outperformed all major fiat currencies from 1900 to December 2019.

The studies looked at the relative value between gold and major currencies – the Indian rupee, the Chinese yuan, the US dollar, the Japanese yen, the British pound, the German mark, the Indonesian rupiah, and the Vietnamese dong. Save for the yen, very briefly in the beginning of the last century, and again for a very short period in the 1920s, no currency has ever managed to top gold in valuation, or even come close.

Over the long term, gold has performed better than other asset classes – given economic vagaries, demand as a means of investment, and low volatility.